Energy geopolitics has entered a new chapter in its long history. Climate change and energy security urge for a shift to renewable energy and other decarbonization options. Such a transition implies big changes to energy systems, markets, and trade flows, and in turn industrial opportunities and political dependencies. The abundance and widespread nature of renewable energy, for example, could ease tensions in what are now oligopolistic oil and natural gas markets. At the same time, global politics shapes the speed and direction of the energy transition. Great power rivalry influences technological choices, trade partnerships, and which global agreements can be reached and enforced. A fast and just transition to a more sustainable energy supply is not assured in world where a multitude of global and regional powers defend their economic and political interests. How will this reciprocal and complex interaction play out? Will the energy transition pacify global (energy) relations or will great power rivalry weaponize the energy transition? While definitive answers are for future historians to give, this brief summarizes the key expectations and considerations regarding the interplay between renewable energy and global politics, sketching the dilemmas countries face while balancing national and collective interests.

New map, new game?

Energy geopolitics is commonly associated with oil and gas security, generally framed as the availability of affordable supply. It focuses on a world in which some countries possess certain resources while others try to get access to them. It paints the picture of oligopolistic global markets where importers hold strategic reserves, diversify imports in terms of sources, origins, and routes, and work with diverse contract portfolios, and where exporters try to generate as much revenues from exports as possible and share an interest in safe transport infrastructure with importers.

Over the last decade, the transition to renewable energy and other decarbonization options has started to reshape the energy map, through investment patterns and directly. The geographic and technical characteristics of renewable energy sources like solar, wind, biomass, geothermal, and hydropower are very different from those of coal, oil, and natural gas. Sources are abundant, widespread, but intermittent (most). Generation requires critical minerals and metals and lends itself to decentral generation. Transportation is generally electric in nature, not as solids, liquids or gases, as most renewable energy sources are directly transformed into electricity, with notable exceptions being hydrogen and bioenergy. There is also a host of other decarbonization options available in the form of nuclear energy, efficiency measures, home insulation or CCS that support transition efforts.

The energy transition represents a new chessboard on which countries play. Scholarly attention has hence focused on the question whether this implies a new game as well, i.e. what the geopolitical implications of the energy transition are. By and large, roughly eight clusters of expectations stand out (Scholten and Bosman 2016; Scholten 2018, 2023; Scholten et al. 2020; Hafner and Tagliapietra 2020; Vakulchuk et al. 2021; Blondeel et al. 2021; IRENA 2019; and many others).

First, renewable energy brings about more symmetrical energy relations in the long run. As all countries have access to some form of renewable energy, most will be able to source a greater share of their energy needs domestically. While the extent depends on domestic capacity, the distinction between exporters and importers blurs, creating ‘prosumer countries’ that have a make or buy option. Add to this that there are also more countries that can act as potential exporters, and we see the shaping of a buyers’ market. Trade volumes of energy sources are likely to drop considerably, reducing energy security and import dependence concerns. Intermittency will, however, create challenges for grid balance and price stability, making availability at the right time a strategic interest.

Second, electrification is likely to lead to regional communities and grid politics in the long run. Electricity suffers from long-distance losses and knows stringent operational requirements due to expensive storage and on the spot balancing of supply and demand to prevent cascading effects. The former, together with the abundance of renewable energy, favors country sized grids or continental connections at most, not global interconnection/trade. The latter implies that pipeline politics turns into grid politics, with emphasis being on where interconnectors should be built, who owns and controls the grid, flows, and storage facilities. Hydrogen is interesting in this regard as it would allow more long-distance trade and would act as a source of diversification from an overreliance on electricity as the main future energy vector. This could be convenient for those countries having less trust in their neighbors.

Third is an increasing struggle for access to critical minerals and metals and limiting supply chain dependencies by moving their processing (closer to) home. Currently, copper, nickel, cobalt, lithium, and rare earths markets are dominated by a few countries (Chile, Indonesia, DRC, Australia, and China respectively according to the International Energy Agency (IEA 2021) while processing is strongly dominated by China across all materials. This issue is especially poignant in the coming two decades when most new capacity has to be installed. The issue differs from oil and gas imports though, as it represents a stock (not a flow), and offers options for recycling and the use of alternatives.

Fourth is a decentralization of energy production. Some renewable energy sources are very scalable, e.g. solar panels, and are likely to be generated closer to home. This changes the way current energy infrastructures operate and can empower local communities away from a reliance on energy companies and transmission grids. It can, however, also provide separatist areas with their own energy sources, strengthening their cause. It is also here where an important question lies regarding the look of future energy systems. The question how much energy will be generated and distributed centrally vs decentrally, together with the question how much alternatives to electricity we will use (new forms of heat like hydrogen, biogas, district heating), are the key question facing policy makers and grid operators in planning future energy systems. Estimates for final energy consumption across end-use sectors range around 20-25% molecules next to 75-80% electricity according to the HydrogenCouncil and McKinsey (2021), but also depends heavily on countries’ climate and industrial needs.

Fifth and sixth, the energy transition is a major and global force of creative destruction. It represents the rise of a new clean tech industry which is coveted by many nations for potential revenues and jobs and that features dominantly in national industrial strategies (e.g. US, EU, China, India, Japan). This competition is already ongoing with China leading in all things electric (solar, wind, batteries, EVs) and OECD countries in molecules (hydrogen, CCS, bioenergy) if we were to sum it up in one sentence. At the same time, the energy transition represents the decline of fossil fuels, leading to potential socio-political instability in exporting countries that rely heavily on their rents. While oil and natural gas are not disappearing anytime soon, and demand for oil based products is likely to remain even longer, it does raise the question how exporters will respond. Will they stall the oil end-game, invest in clean fossil, or diversify their economy towards renewables or something else? In any case, those countries that produce at lowest cost per barrel, mostly the Middle East, will be the last to need to switch. Moreover, rising energy demand in the global South is likely to offer new export opportunities for them while the global North is decarbonizing.

Seven, non-renewable decarbonization options such as nuclear energy, efficiency measures, home insulation, and CCS help to reduce CO2 emission in the short term but risk carbon lock-in in the longer term. Especially, the so-called hard-to-abate sectors such as the heavy industry, the chemical industry, heavy transportation, and heat will likely be relying on fossil fuels longer and decarbonize through hydrogen and CCS. Once these technologies are installed, they will not be easily replaced. Moreover, it is not certain that green hydrogen through electrolysis will come down in costs soon.

Finally, and perhaps most importantly, the energy transition produces winners and losers. Not all countries can and will move equally fast nor benefit equally from this transition. Some will turn their oil and gas import dependence into clean energy technology exports while others will simply replace fossil imports for clean tech imports. Current oil and gas exporters will also need to manage to diversify. However, to enjoy the economic, security, and climate benefits of renewable energy, the transition needs to be fast and just. Fast, for otherwise we will incur climate damages. Just, for we need everybody on board to limit climate change. So far, countries’ emphasis has been on national strategies to ‘win’ the transition game, far less attention has gone to achieving collective benefits and ensuring a smooth global energy transition. The role of international organizations such as OPEC, OECD, UN, IRENA, etc. in providing some form of global energy governance will be interesting to keep an eye on in this regard.

In the end, the geopolitical implications of the energy transition are a matter of two steps forward and one step back, or, if we put it in a temporal perspective, one of a challenging transition with the light at the end of the tunnel. It is also a move form concerns about energy sources to energy carriers and technologies, i.e. from sources to distribution and supply chains.

New trends, new game?

Energy (security) policy is a complex two-level game. On the one hand, domestic possibilities and politics determine energy strategies with attention turning abroad afterwards for whatever countries need to import or wish to sell. On the other hand, global politics sets parameters for policy priorities and trade possibilities. A number of trends deserve attention in this regard.

First and foremost is the trend of increasing great power rivalry. If the Cold War was marked by bipolarity, the 1990s and early 2000s by unipolarity, we are now in a phase where China’s economic and increasingly military rise is challenging US hegemony, but where many regional powers such as the EU, Japan, India, Russia, and Brazil are also repositioning themselves. It is bipolar in some ways, with the US and China leading the camps, and multipolar in others, while managing Thucydides’ trap seems key to stabilizing global relations. In such a setting, energy is but one of many areas in which states compete and where energy itself can be instrumentalized to serve other political purposes. States may consider industrial competitiveness and military supremacy more important than clean energy and use energy as a way to harm potential rivals, as we have seen between Russia and the EU.

Another trend is that of increasing climate change, environmental degradation and resource depletion. The effects of past CO2 emissions are increasingly noticeable and the Paris Agreements’ 1,5°C target is out of reach despite actions having lowered projections from 4 degrees to 2,5-3 degrees Celsius by the end of the century (Climate Action Tracker 2023). The need to phase-out fossil fuels is largely driven by climate change concerns, not so much the scarcity of fossil fuels as was long feared. Currently, it is expected that there are 50 years of natural gas reserves, 60 years of oil reserves, and 140 years of coal reserves left at current consumption levels and known reserves (Energy Institute 2023). Instead of peak oil, we face peak demand. As a result, the push for an energy transition is to a great extent driven by countries’ perceptions of climate change.

A third trend, and more directly related to energy, is that global energy demand is shifting towards the Global South due to a combination of population growth and economic development (IEA 2018). It will be of importance how they intend to meet demand, e.g. through renewable energy for sustainability reasons or fossil fuels as they are proven and readily accessible for industrialization (Scholten 2024 forthcoming).

The result of this complex two-level game is that energy policy and global energy politics is marked by great diversity and many players. If we were to shamelessly generalize, we might sum up global dynamics in the following way. The Global North, by and large, sees renewable energy as a means of diversification away from fossil fuels and as a key aspect of industrial policy, i.e. as an engine for jobs and exports. They are set to compete over market shares while sharing a collective interest in abating climate change. The Global South sees in the energy transition a means to increase energy access and economic development, where they can sell own resources and materials and move up the value chain in a way they could not with fossil fuels. While they are relatively strongly affected by climate change, they lack the finance to green their energy sector and might opt for cheap fossil fuels instead. For fossil fuel exporters, like OPEC and Russia, the energy transition threatens their main revenue stream and domestic stability. They hence strategize how to cope with an eventually declining sector as mentioned earlier, but are likely to compete with renewable energy technology exports on the short term.

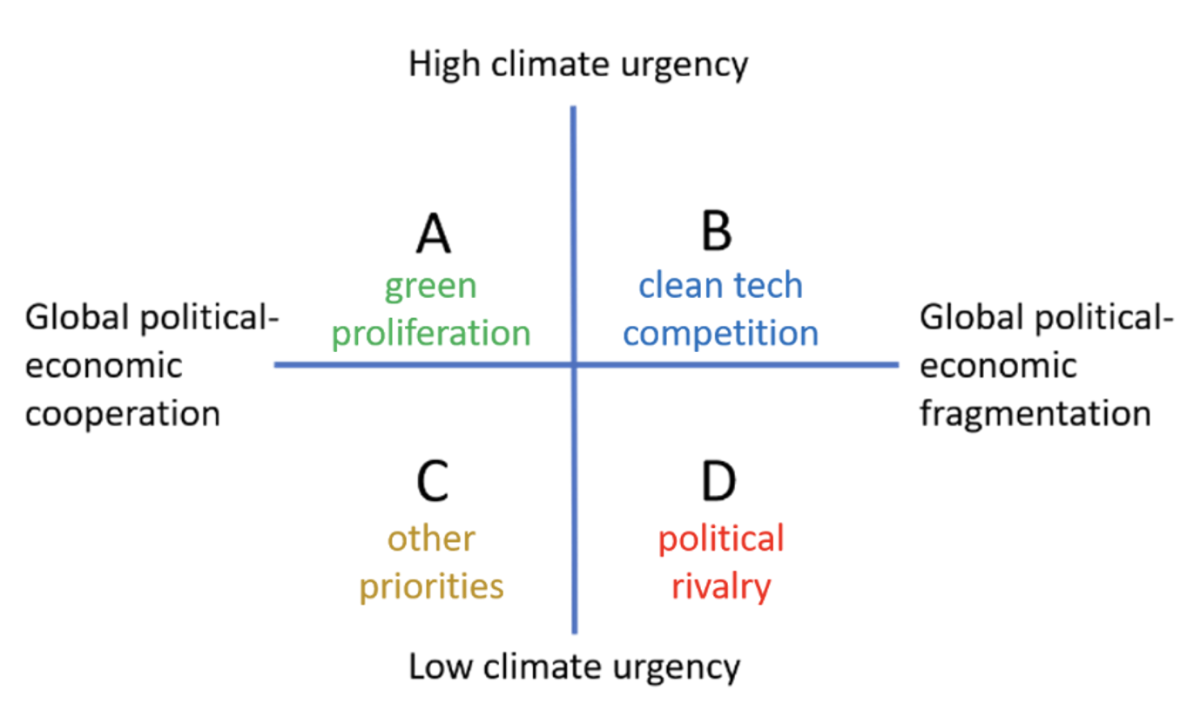

The diversity of trends and actors makes it hard to estimate the outcome of that interaction. In such situations, scenarios can be a helpful tool to reduce complexity to manageable proportions. The combination of great power rivalry and (perceived) climate urgency can be taken as the two core uncertainties in global energy security scenarios and strategic thinking, though clean technology breakthroughs have been used instead of climate urgency (Goldthau et al. 2019). It has also proven valuable time and again in my own courses on the geopolitics of the energy transition. By and large, we can paint four scenarios based on these two uncertainties and derive consequences for the speed and direction of the energy transition from them (see Figure 1).

Scenario B (clean tech competition) is what most would consider the current trajectory. It represents a world with a strong need for climate action (mitigation) that is increasingly politically fragmented. It is a world where rivalling great powers develop clean energy technology in a setting of strong economic competition and through protectionist if not downright mercantilist ways. This leads to a fast uptake of renewable energy in those countries ‘winning’ this competition and those aligned to them, but a slow fossil fuel phase-out in those areas likely to ‘lose’ industrially in this energy transition. If trade becomes strongly politicized, it may only occur between certain countries and/or withing certain regions or blocks.

Scenario C (other priorities) resembles the opposite of scenario B. It represents a future world of economic globalization through cooperation and global institutions, possibly under hegemonic guidance. Climate action is not a top priority as either climate impacts will be dealt with through adaptation (and not mitigation) or other, socio-economic issues, have priority. This leads to trade in both fossil fuels and renewable energy, with clean technologies seen as industrial opportunity but where rivalry is managed through markets and global institutions. Both the uptake of renewable energy and phase-out of fossil fuels are medium.

Scenarios A and D represent the two extremes. Scenario A (green proliferation) represents a world that strikes a ‘renewable energy proliferation treaty’ to mitigate climate change as global cooperation enables joint action while climate change impacts are either felt or perceived as the main policy issue. In essence, a compromise will be found between concerns in the Global North about energy and material security, protection of intellectual property rights, and industrial opportunity and worries in the Global South about finance, know-how, and economic development, while forms to compensate fossil fuel exporters or means to co-opt them in the energy transition have been found (e.g. hydrogen). The transition to renewable energy progresses very fast while fossil fuels are phased out fast.

Scenario D (political rivalry), finally, represents a world where great power rivalry overshadows climate concerns and countries focus on climate adaptation and securing energy through whatever means necessary. Emphasis is on using all available domestic sources in a setting of politicized supply chains (e.g. critical materials). Dependence on foreign supplies, especially from rivalling countries, is avoided, making some turn to domestic fossil fuels and others to renewable energy. This leads to a slow or fast uptake of renewable energy depending on countries’ resources, but a medium one overall, and slow phase-out of fossil fuels.

Overall, the impact of global politics on the speed and direction of the energy transition is bigger in times of strong great power rivalry. When economic competition and military threats become imminent, countries cannot sacrifice short term goals for long term benefits. Only direct global climate catastrophe might lead to a ‘ceasefire’, but by then, of course, it is already too late climate wise. In this sense, scenario B still offers some hope, but we must make sure not to have great power rivalry escalate further, so as not to end up in scenario D.

Achieving the Security Benefits of Renewable Energy

We started this brief by asking how the interaction between the energy transition and global politics would play out. Will the energy transition pacify global (energy) relations or will great power rivalry weaponize the energy transition? Looking at the 8 expectations and 4 scenarios, and viewing energy geopolitics as a two-level game, the answer is a bit of both. Global politics is likely to determine the speed and direction of the energy transition in the short run while renewable energy sources and technologies will reshape energy relations from the ground up in the long run. In that sense, renewable energy depoliticizes global (energy) relations over time by leading to end stage where energy self-sufficiency is greater than currently, while political competition will heighten the transitional challenges noted, e.g. access to critical materials and industrial rivalry. While it is hard to imaging global politics derailing the entire energy transition, as sooner or later we will run out of fossil fuels, climate damages will force us to ask a follow up question: how to ensure a smooth global energy transition?

A smooth global energy transition rests on understanding the complex interplay between (changes in) energy systems and global politics and finding ways for policy makers to balance national energy security and industrial interests with collective climate and stability concerns. Much research has to be done on this front, both conceptually and empirically, but also explicitly on possibilities for more global energy governance. Regarding the latter, the framing of renewable energy as having national and global security benefits next to global climate and national economic advantages seems a first step in this regard. Historically, global energy governance has only truly emerged in those instances where energy and military security were related, e.g. nuclear non-proliferation and the European Coal and Steel Community. A second step would then be a renewable energy proliferation treaty that manages to balance the interests of the Global North, Global South, and fossil fuel exporters, as mention earlier. Such things are of course much easier to write than to do, but something along those lines is required to ensure that the energy, climate, and security benefits of renewable energy are to be realized during and not only after the transition.

Figure 1. Four Scenarios on the Geopolitics of the Energy Transition

References

Blondeel, M., M. Bradshaw, G. Bridge and C. Kuzemko. 2021. The geopolitics of energy system transformation: A review. Geography Compass. DOI: 10.1111/gec3.12580.

Climate Action Tracker. 2023. December 2023 Update. Available at: https://climateactiontracker.org/global/temperatures/.

Energy Institute 2023. Statistical review of world energy. Available at: www.energyinst.org/statistical-review.

Goldthau, A., K. Westphal, M. Bazilian and M. Bradshaw. 2019. How the energy transition will reshape geopolitics. Nature, 569, 29–31.

Hafner, M. and S. Tagliapietra (Eds.). 2020. The Geopolitics of the Global Energy Transition. Cham: Springer Nature.

HydrogenCouncil, & McKinsey. (2021, February). Hydrogen Insights, A Perspective on Hydrogen Investment, Market Development and Cost Competitiveness. Available at: https://hydrogencouncil.com/wp-content/uploads/2021/02/Hydrogen-Insights-2021.pdf

International Energy Agency (IEA). 2018. World energy outlook 2018. www.iea.org.

International Energy Agency (IEA). 2021. World energy outlook 2023. www.iea.org

International Renewable Energy Agency (IRENA). 2019. A New World – The Geopolitics of the Energy Transformation. Report by the Global Commission on the Geopolitics of Energy Transformation. Abu Dhabi: IRENA.

Scholten, D. and Bosman, R. 2016. The geopolitics of renewables; exploring the political implications of renewable energy systems. Technological Forecasting and Social Change, 103, 273–283.

Scholten, D. and D. Zuckerman. 2024. The Geopolitics of the Global Energy Demand Transition. Forthcoming in the Analyses series of the Elcano Royal Institute, Madrid, Spain.

Scholten, D., Bazilian, M., Overland, I. and Westphal, K. 2020. The geopolitics of renewables: New board, new game. Energy Policy, 138, 111059.

Scholten, D. (Ed.). 2018. The Geopolitics of Renewables. Cham: Springer Nature.

Scholten, D. (Ed.). 2023. Handbook on the Geopolitics of the Energy Transition. Cheltenham: Edward Elgar.

Vakulchuk, R., I. Overland and D. Scholten. 2020. Renewable energy and geopolitics: Literature review. Renewable and Sustainable Energy Reviews, 122, 109547.

Further Reading on E-International Relations